Government borrowing could respond to intertemporal allocation of public resources to smooth expenditure, investment, and taxation. It allows expediting the investment process to foster economic growth and helps in economic stabilization.

According to Eichengreen et al. (2019), sovereign debt has a long history with evolving nature and dynamics. Debt before the 19th century was mainly used to secure borders, prosecute wars, and heighten chances of state survival. In the 19th century, war financing continued to be important, but with stronger states, spending shifted towards the provision of additional public goods such as infrastructure development of water and sewer works, railroads, ports, canals, and public education. Debt in the 20th century resulted from major wars, recessions, banking panics, and financial crises and the public-policy responses to those events, and from increasing economic development initiatives led by national governments. Meanwhile, Yared (2019) points out that in the last four decades, debt has increased because of an aging population, rising political polarization, and rising electoral uncertainty that have pushed towards granting pensions, health care, and other often unfunded social services. To keep debt over GDP under control, the economy must grow faster than the financial costs and/or ordered fiscal balances must guarantee intertemporal solvency.

A government could finance its operations with loans and bonds, in domestic and international markets, and negotiated in domestic and foreign currency. The debt management strategy requires covering the funding needs at the minimum borrowing costs with an acceptable level of risks, recognizing that there is a cost-risk trade-off.

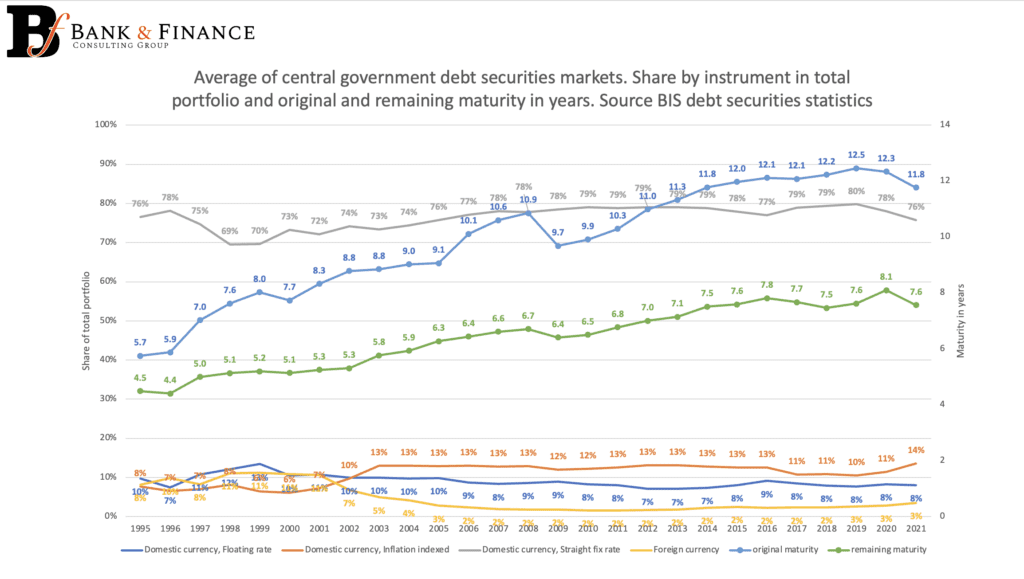

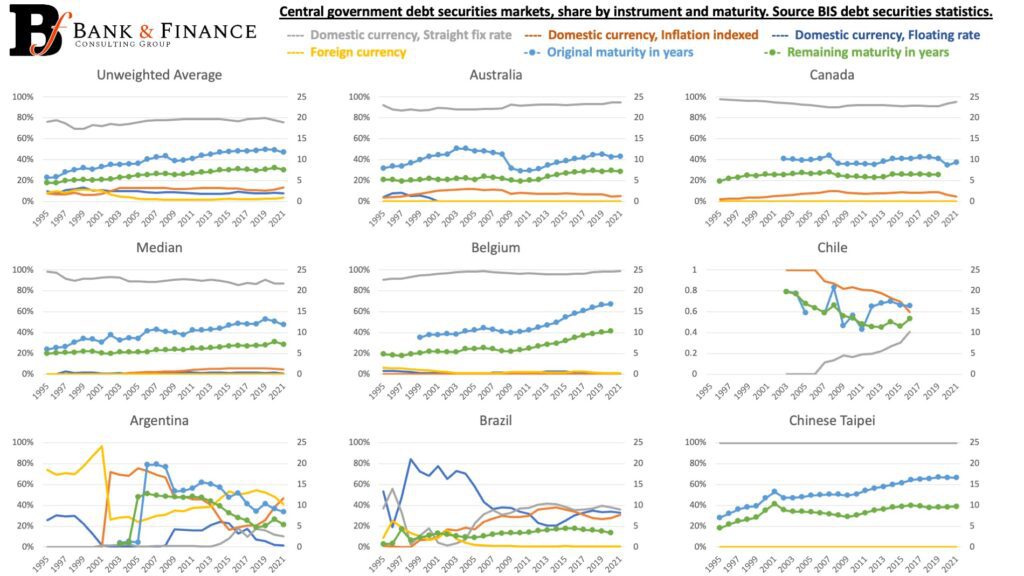

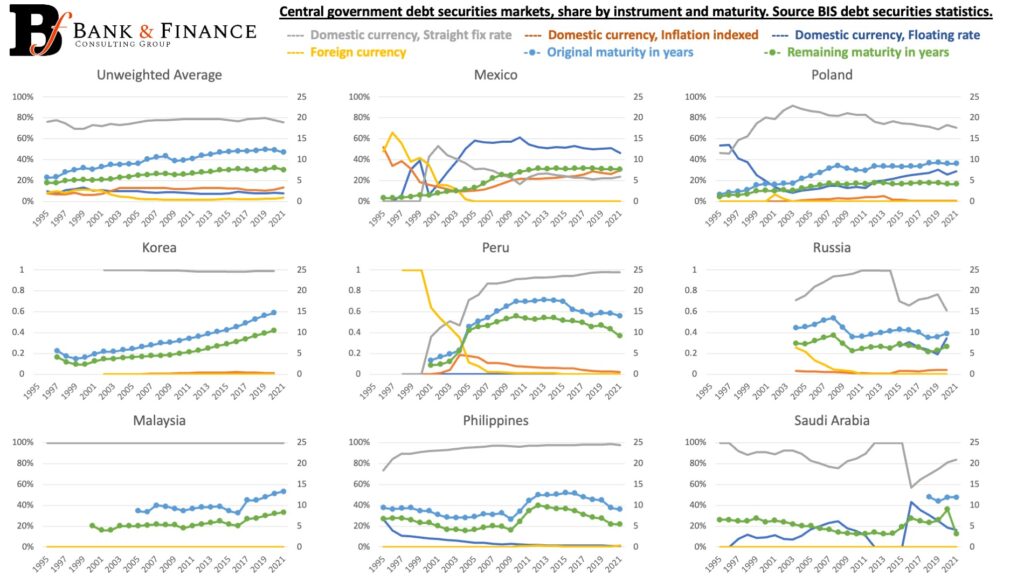

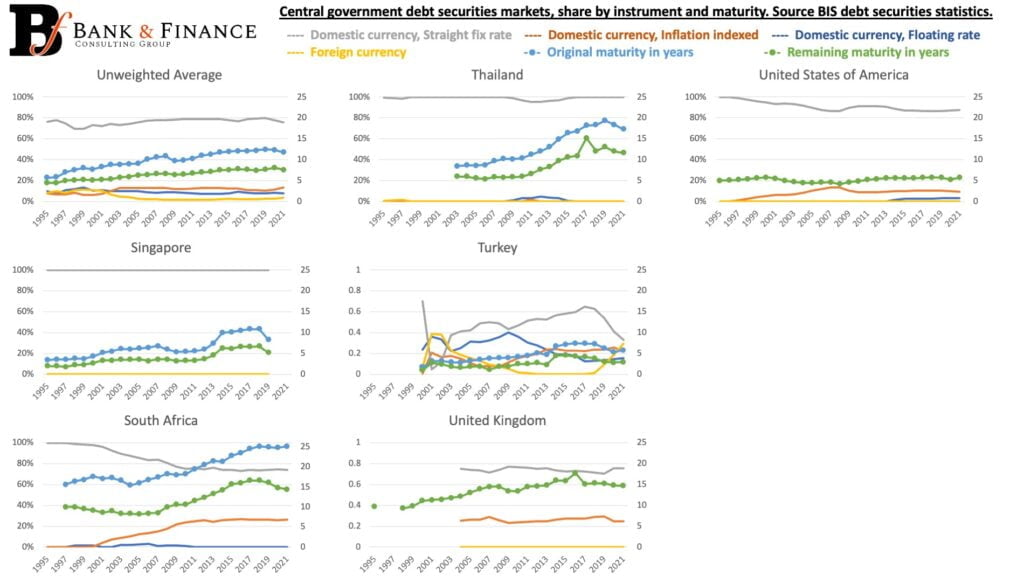

Using information from the debt securities statistics, published by the Bank of International Settlements, it is possible to analyze the type of debt instruments issued by 30 central governments around the world from 1995 to 2021. Below we report the share of domestic and foreign currency debt in the portfolio, where for domestic currency debt we distinguish between straight fix rate, inflation indexed, and floating rate. We also report the original and remaining maturity of the debt securities. We report the unweighted average, the median and the shares by security type of each country, along with the maturity. From the data we can observe that:

1) There is heterogeneity in the composition of debt portfolios across countries.

2) Most of the debt is in domestic currency with a straight fix rate.

3) The second most prominent instrument type is domestic currency inflation indexed, which is important in Argentina, Brazil, Chile, Colombia, Hong Kong, Israel, Mexico, South Africa, Turkey, the United Kingdom and the United States.

4) Argentina, Brazil, Hungary, Indonesia, Israel, Philippines, Poland, Russia, and Turkey, which have contracted domestic currency debt at a floating rate, have been reducing the share of this type of debt in their portfolio. Mexico is the only country where this type of debt has the largest share in its portfolio.

5) Foreign currency debt continues to be important in Argentina and Turkey, while other emerging market countries, which used to issue foreign currency debt have been successful substituting towards domestic currency debt.

6) Average original maturity has been increasing from 5.7 years in 1995 to 11.8 years in 2021, while remaining maturity increased from 4.5 years in 1995 to 7.6 years in 2021. Maturity has been increasing in most countries.

In the current inflationary environment, which is forcing central banks around the world to increase interest rates to anchor inflation expectations, inflation indexed and floating rate debt instruments are increasing governments’ financing costs.

As proposed by Jonasson et al. (2019), monitoring and management of risks requires observing the maturity structure, the unhedged exposures, the optionality and derivatives, the cancellation and acceleration clauses, and the contingent liabilities. Reducing funding risk and variability in interest costs are debt management sound practices to promote debt sustainability. It will be important to monitor how inflation and increasing interest rates affect the expanding debt levels registered in the last years in response to COVID-19.

References

Eichengreen, Barry, El-Ganaiyu Asmaa, Pedro Esteves Rui and Mitchener Kris James (2019). Public Debt through the Ages. In S. Ali Abbas, Alex Pienkowski and Kenneth Rogoff, editors, Sovereign Debt: A Guide for Economists and Practitioners, Oxford University Press.

Jonasson, Thordur , Mike Williams, Michael Papaioannou (2019). Debt Management. In in S. Ali Abbas, Alex Pienkowski and Kenneth Rogoff, editors, Sovereign Debt: A Guide for Economists and Practitioners, Oxford University Press.

Yared, Pierre (2019). Rising Government Debt: Causes and Solutions for a Decades-Old Trend. Journal of Economic Perspectives, 33: 2.