In this research paper, we show the importance of considering non-linear effects when analyzing macroeconomic and financial linkages. The main reason is that the relative importance of financial conditions over economic allocations is not constant over time. When financial markets are functioning correctly, economic criteria is the main determinant of resources allocations, but when there is financial stress, finance could become the main determining factor. In addition, we show the role that monetary policy could have in periods of financial stress. The evidence on this paper is provided using post-1962 data from the United States, where several episodes of financial calm and stress are analyzed.

This paper is part of a wider research agenda, where we have been analyzing the importance of considering non-linear factors when modeling monetary policies, fiscal policies, aggregate supply of goods and services, inflation, and exchange rate dynamics in emerging markets economies, which are more prone to non-linear dynamics.

The technical work in this paper consists of performing Bayesian estimations of Markov-switching Vector Autoregression (MS-VAR) and and Markov-switching Dynamic Stochastic General Equilibrium (MS-DSGE) models to analyze the advantages of allowing Markov-switching in coefficients / parameters and variances / shocks. An advantage of the VAR framework is that it imposes less constraints on the estimation. An advantage of the DSGE one is that it could provide economic interpretation of what is estimated.

Based on Maximum Likelihood criterion, the introduction of Markov-switching improves the models’ fit to the data. An estimated time-invariant DSGE produces larger shocks relative to a DSGE model with Markov-switching in parameters. An estimated DSGE without Markov-switching in parameters misinterprets structural regime switches as large shocks events. Meanwhile, an estimated DSGE without Markov-switching in shocks overestimates the high coefficient regimes. The impulse response functions are markedly different depending on the regime the economy is under.

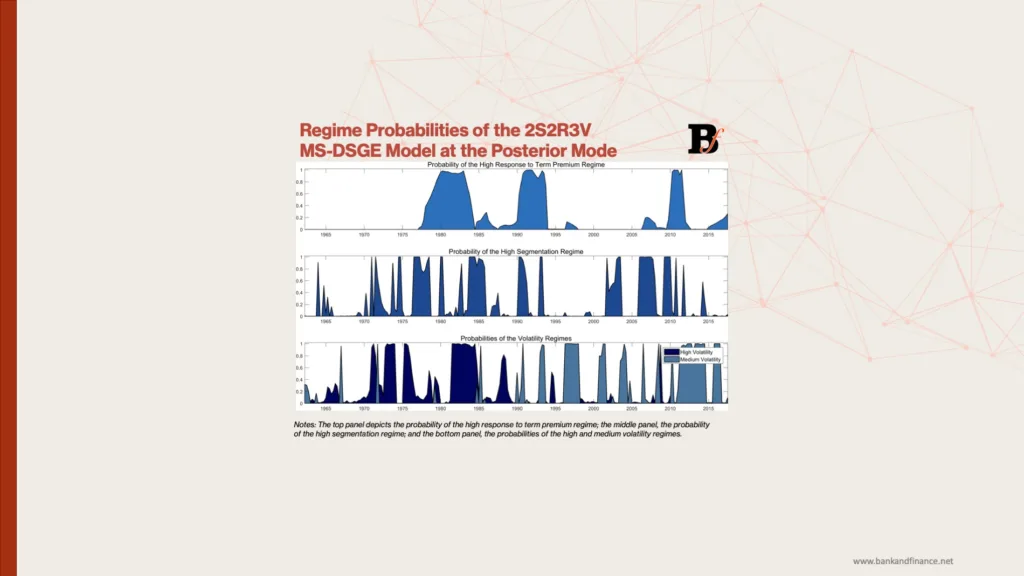

Using the MS-DSGE model specification with the best fit to the data, we: (i) provide evidence on how financial conditions have evolved in the US since 1962, (ii) show how the Federal Reserve Bank has responded to the evolution of term premiums, (iii) perform counterfactual analysis of the potential evolution of macroeconomic and financial variables under alternative financial conditions and monetary policy responses.