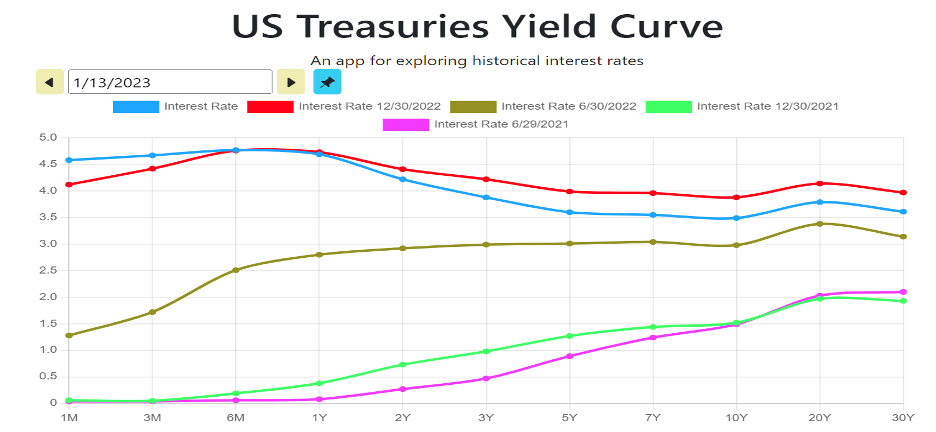

A yield curve provides information about prevailing interest rates for debt securities of different tenors (say one month, three months, one year, ten years, etc.) at a particular point in time (say today or six months ago). Usually, a yield curve reports information from a single issuer, say a country’s Treasury, where factors affecting the risk structure of interest rates, as default risk, liquidity and income tax considerations, are held constant. Here is an example of the current yield curve for US Treasuries and those prevailing at the end of the last 4 semesters.

Through a no-arbitrage condition, interest rates of different tenors are expected to be related as bonds of different maturities are substitutes and their expected return should be equalized. This explains why interest rates of different tenors move together as shown in the next figure. In addition, yield curves are usually upward sloping as longer maturity bonds usually have higher interest rates as observed in the same figure.

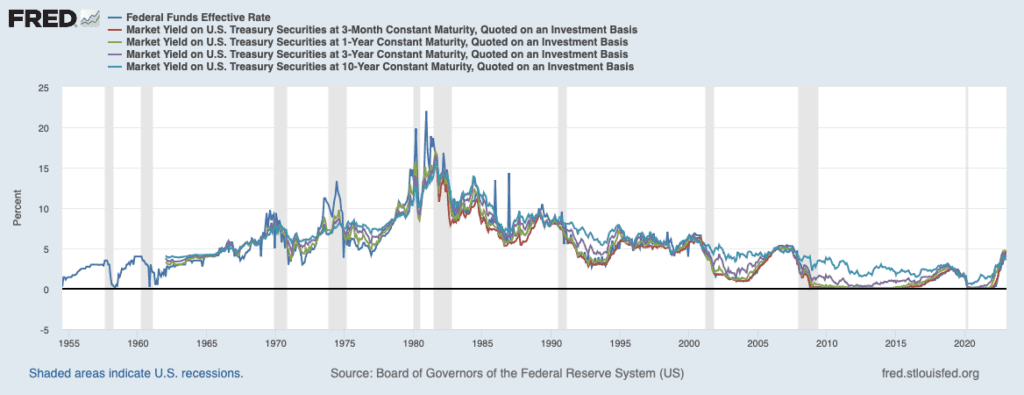

The difference between today’s interest rates for different tenors is mainly related to the expected short-term interest rates prevailing in the future and the term premium. The term premium is the extra compensation required by investors for bearing interest rate risk associated with those short-term yields not evolving as expected. Next figure shows that U.S. term premiums from 1990 to 2007 were always positive, but in 2008 we started observing negative term premiums for one-year bonds and in 2011 ten-year bond registered its first negative value, which has been more common during periods of monetary expansion.

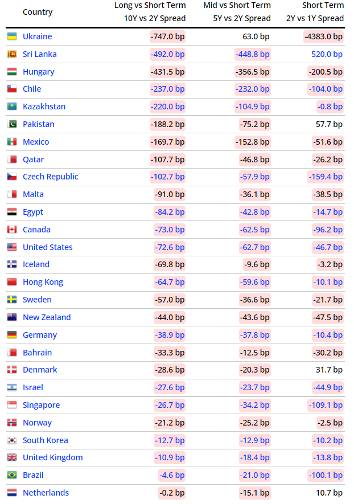

According to http://www.worldgovernmentbonds.com/ as of 16 January 2023, the following 27 countries have inverted yield curve with the following spreads among tenors.

An upward sloping yield curve is an interest rate environment in which long-term bonds have a higher yield that short-term ones, it signals that short-term rates are expected to increase in the future and could signal forthcoming inflation. On the other hand, a downward sloping, or inverted yield curve is an interest rate environment in which long-term bonds have a lower yield than short-term ones, it signals that short-term rates are expected to decrease in the future, is often considered a predictor of economic recession. The attached presentation, based on Frederic Mishkin and Stanley Eakins “Financial Markets and Institutions”, provide the fundamentals on yield curves.